[Retirement Pension Strategy for Office Workers in their 40s] Why You Should Switch from DB to DC (ETF Management)

Even for a senior manager at a large corporation earning 120 million KRW annually, faced with stagnant annual wage increases of 1-3% and the reality of high inflation, real purchasing power is continuously declining. Relying solely on the company’s existing retirement pension system for the remaining 10 years until retirement is tantamount to neglecting the risk of asset value depreciation, and defending against inflation and actively pursuing asset growth is now an essential investment challenge for survival.

Through this article, readers will gain three key insights today :

[Redefining Retirement Pension Structure] Clearly understand the fundamental differences between Defined Benefit (DB) and Defined Contribution (DC) retirement pensions, and establish criteria to determine which choice can protect the real value of your assets by comparing your wage growth rate with market returns.

[Inflation Defense Strategy] Understand the necessity of a core Exchange Traded Fund (ETF) portfolio strategy that can transform your retirement savings from a simple arithmetic guarantee into an investment asset, amidst consumer prices rising 2-3% annually and the threat of asset erosion.

[Compounding of DC Management Returns] Confirm with real-world data the dramatic difference in retirement assets created by the gap between stagnant annual wage increases and aggressive DC (ETF Management) returns.

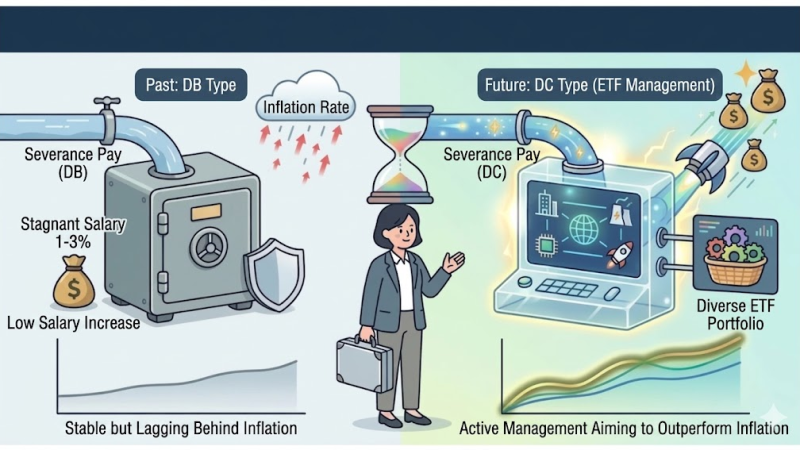

[Onboarding] [Retirement Pension System : DB vs DC]

Retirement pensions are the most basic asset for preparing for old age, but the size of your retirement fund 10 years from now will differ dramatically depending on who holds the initiative in its management.

Defined Benefit (DB) is a structure where the company manages the retirement fund, and you receive a payment calculated according to a fixed formula (average salary over the last 3 months before retirement × years of service) upon retirement. While the company bears all responsibility for management, any market boom’s profits belong entirely to the company, and you cannot enjoy returns beyond the predetermined amount.

Conversely, Defined Contribution (DC) is a system where the company annually contributes a fixed amount to your account, delegating the responsibility and authority of management to you. This is an opportunity for you to become the primary manager of your assets and capture market returns in your retirement fund account. A powerful investment tool that emerges in this process is the Exchange Traded Fund (ETF). An ETF is a product that bundles a specific market index or asset class and trades in real-time, offering an efficient tool to diversify risk compared to individual stock investments while stably tracking average market returns.

| Category | Defined Benefit (DB) | Defined Contribution (DC) |

|---|---|---|

| Management Entity | Company | Employee |

| Management Responsibility | Company | Employee |

| Amount Received | Average salary over the last 3 months before retirement × years of service | Contributions + Investment Returns |

| Investment Tendency | Stable (Principal protection-oriented) | Aggressive (Utilizes investment products) |

| Recommended For | Employees with high wage growth rates | Employees seeking market returns |

DB vs DC / Retirement Pension : DB vs DC

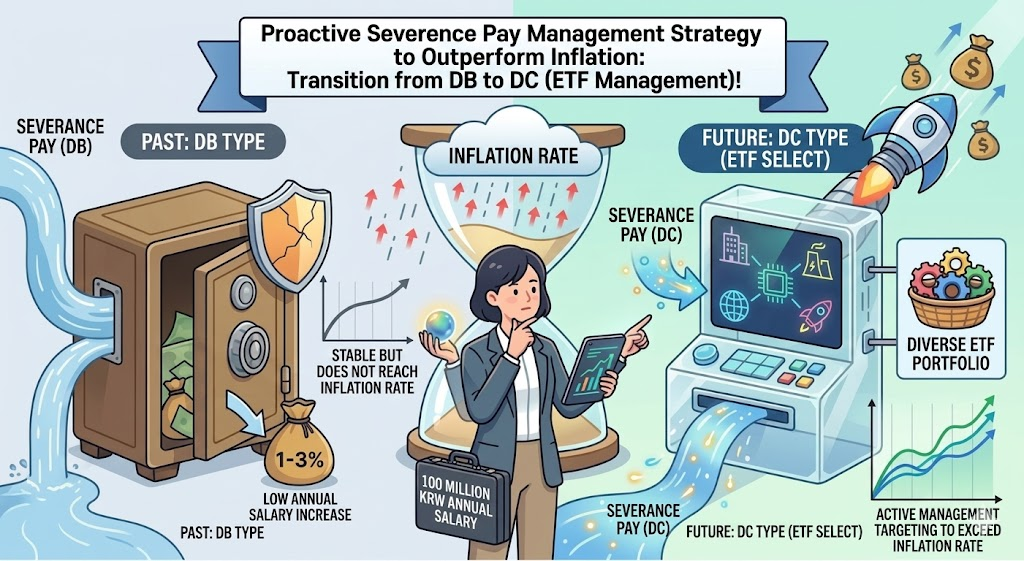

Investment Point: While DB is advantageous when wages rise sharply at retirement, it is crucial to recognize that wage growth rates in an era of low growth cannot keep pace with the speed of asset accumulation.

1. Macroeconomic Environment : Inflation Rate and the Threat to Real Purchasing Power

The fundamental reason we must switch to a DC-type retirement pension and actively manage it is the decline in real purchasing power. In recent years, global inflation has silently eroded the assets of employees with low annual salary growth. Below is the trend of average annual consumer price inflation over the last three years in major countries.

| Year | 2% Annual Salary Increase | Korea Inflation 2.7% | US Inflation 3.1% | EU Inflation 3.7% |

|---|---|---|---|---|

| 1st Year | 122 million | 123 million | 124 million | 124 million |

| 5th Year | 132 million | 137 million | 140 million | 144 million |

| 10th Year | 146 million | 157 million | 163 million | 172 million |

Data source: IMF World Economic Outlook Original Source

If your annual salary increase merely stays at 2%, you can see that the purchasing power of your retirement assets will continuously erode in a high-inflation environment. To maintain the current value of your retirement fund, asset allocation that generates returns at least exceeding the inflation rate is absolutely essential.

As shown in the table above, the moment your annual salary increase falls below the inflation rate, the real purchasing power of your retirement fund continuously declines. Leaving your retirement pension in a DB-type plan is like passively accepting the attack of inflation. Without asset allocation that yields returns at least exceeding the inflation rate, your retirement will inevitably be far more meager than before.

Key Metric: Calculate the difference between the consumer price inflation rate and your annual salary increase rate. That difference signifies that your assets will be poorer in real terms 10 years from now than their current value.

http ://googleusercontent.com/image_generation_content/174

10-Year Inflation Projection / 10-Year Inflation Simulation

Key Metric: Check the gap between national inflation rates and your own annual salary increase rate. An annual return of at least 3% is required to protect the real value of your assets. Statistics Korea Report

2. Investment Strategy : Volatility Control and Upward Trend Strategy Using ETFs

If you’ve switched to a DC plan, you now need to formulate a strategy for how to grow your assets. In the reality of stagnant wage increases for those in their 40s, retirement fund management returns are the sole engine to support your old age. The key is to select broad market index-tracking ETFs that reduce volatility while allowing you to benefit from market growth.

The S&P 500 (Standard & Poor’s 500) or Nasdaq 100, which represent the U.S. market, are proven tools that reliably provide average market returns for long-term investments. For those in their late 40s, allocating 70% to equity ETFs and 30% to bond ETFs to control volatility, and performing annual rebalancing in response to changing market conditions, can dramatically improve long-term returns.

Related Resources: U.S. Asset Allocation Strategy

Investment Point: Do not waste emotions on the stock price fluctuations of individual companies. Building a system where your entire asset portfolio trends upward together through market index-tracking ETFs is the essence of asset management.

3. The Magic of Compounding : Analyzing the Return Gap Between Salary Increase vs. DC (ETF Management)

From the perspective of an employee receiving stagnant annual salary increases (1-3%), it’s crucial to compare with data why DC (ETF management) returns are important. While retirement funds increase arithmetically when salaries rise by 2% annually, managing ETFs that achieve an average annual return of 6% in a DC account creates an overwhelming difference due to the compounding effect.

| Category | Stagnant 2% Annual Salary Increase (DB-type) | DC (ETF Management) 6% Annual Return |

|---|---|---|

| After 1 Year | 1.02x | 1.06x |

| After 5 Years | 1.10x | 1.34x |

| After 10 Years | 1.22x | 1.79x |

Return Gap Comparison

Enjoying market returns through a DC (ETF management) plan in an employee’s retirement pension account is not merely a financial technique. An annual management return of 6%, surpassing the inflation rate, creates a gap in asset value of approximately 46% or more compared to a DB-type plan after 10 years. The magic of compounding ultimately occurs when higher returns are reinvested over a longer period, which is the core of the financial resolve behind switching to a DC plan.

Key Metric : Do not settle for stagnant annual salary increases. The magic of compounding truly begins to work when you set a target return rate of 6% or more and maintain a DC (ETF management) portfolio.

Next Step

For a senior manager in their 40s to successfully conclude their career, now is the golden time for change.

Metrics to Check: Compare your company’s retirement pension regulations, average wage increase rate over the last 5 years, and pension management returns.

Actions to Take: Confirm the possibility of switching to a DC plan with the HR team, and after opening a DC account, establish an equity/bond allocation strategy.

Key Keywords to Search: Retirement pension DB DC comparison, retirement pension ETF management, pension savings tax credit, tax deferral effect, rebalancing strategy.