Structural Design of Retirement Assets : A Perfect Retirement Portfolio Strategy from the 1st to 4th Floor

Securing a monthly cash flow of 5 to 8 million KRW after retirement goes beyond merely having numbers in a bank account. It’s about generating the same level of economic value as owning a ‘small building’ worth billions of KRW and receiving stable monthly rental income. However, most of us rely on finite income in the form of salaries from labor. Labor income inevitably ceases upon retirement. When that day comes, we should have already completed ‘our own building.’ If we don’t start constructing our retirement building now through multi-layered pension and investment strategies, retirement will become a threat to survival, not a period of rest.

Through this article, readers will gain exactly three key insights today:

Asset Layering Strategy: Diversifying risk and securing structural stability for retirement assets through the systematic combination of National Pension, retirement pensions, personal pensions, and individual stocks.

Maximizing Compounding Effect: Enhancing the operational efficiency of pension assets by leveraging time and returns, and accelerating asset growth through tax benefits.

Investment Practice Guide: Establishing an age-specific asset allocation roadmap until retirement, and implementing a proactive asset management strategy that solidifies the underlying structure (pensions) before deploying growth engines (individual stocks) centered on technology-dominant companies.

[Onboarding] Multi-Layered Architecture Strategy for Retirement Assets

Why a Multi-Layered Architecture Strategy for Retirement Assets is Essential

If a building’s foundation is unstable, no matter how elaborately the upper floors are decorated, the risk of collapse cannot be avoided. The same applies to retirement planning. The National Pension, a state social security system, currently faces cracks due to demographic changes and potential uncertainties in benefit payouts, making it dangerous to rely on it as an absolute source.

Risk Diversification: The four-stage structure of National Pension, retirement pensions, personal pensions, and individual stocks diversifies risk, preventing the entire asset portfolio from collapsing simultaneously even in the event of a specific economic crisis.

Income Replacement: At retirement, when labor income ceases, generating a stable monthly cash flow of several million KRW provides economic freedom equivalent to the rental income from a small building worth billions of KRW.

Systematic Approach: If we do not start building our assets with precise engineering design now, we will inevitably face the day when labor income stops empty-handed.

Strategic Response Beyond Wishful Thinking: Prepare Your Own Building (Small Building)

One should not be complacent with temporary improvements in the National Pension’s returns or a numerical increase in its profit size. South Korea is currently experiencing an unprecedented ultra-low birth rate and rapid aging, and its demographic structure is transforming into an extreme ‘inverted pyramid’ shape.

Structural Limitations: The structural pressure of 100 working-age individuals having to support a staggering 83.2 elderly people by 2056 will directly impact the National Pension benefit structure.

Danger of Complacency: Relying on ‘wishful thinking’ that the state will fully take responsibility for one’s retirement is a very dangerous financial gamble.

Building Your Own Structure: Position the National Pension as a minimum defense line, akin to a ‘semi-basement.’ Then, build the framework with retirement pensions and personal pensions, and through the powerful engine of investing in technology-dominant companies, prepare ‘your own economic building (small building)’ starting now.

This content was prepared by referencing data on the National Pension Service Fund Management Status and the National Data Agency’s Future Population Projections.

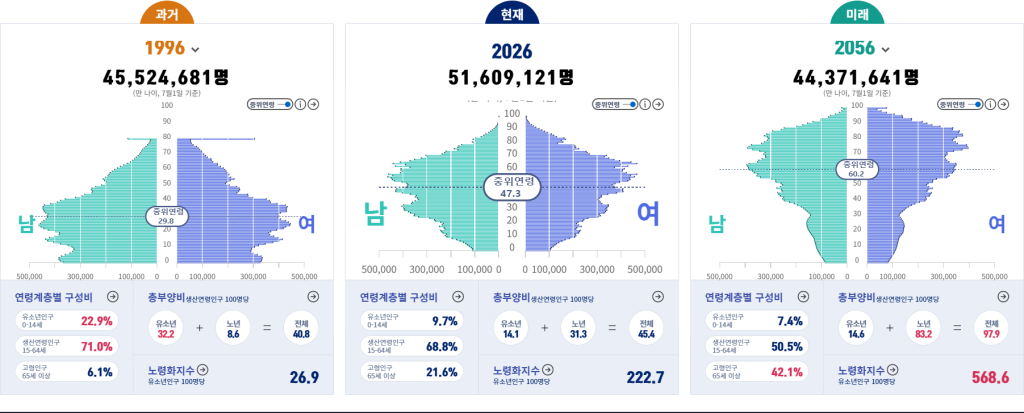

1. South Korea’s Demographic Structure and the Turning Point in Retirement Preparation

South Korea is experiencing an unprecedented ultra-low birth rate and rapid aging globally. According to the attached demographic dashboard data, population changes directly affecting the National Pension benefit structure are very serious:

Inverted Pyramid Demographics: The youth population, which was 22.9% in 1996, has sharply decreased to 9.7% as of 2026, and is projected to fall to 7.4% by 2056. Conversely, the proportion of the elderly population increased from 6.1% in 1996 to 21.6% in 2026, and is expected to reach 42.1% by 2056. This signifies a transformation beyond the traditional ‘urn-shaped’ structure to an extreme ‘inverted pyramid’ shape.

Surge in Dependency Burden: The total dependency ratio (elderly), which indicates the number of elderly people to be supported by 100 working-age individuals, increased from 8.6 in 1996 to 31.3 in 2026. More critically, it is projected to surge to a staggering 83.2 by 2056, meaning 100 working-age individuals will have to support more than 83 elderly people.

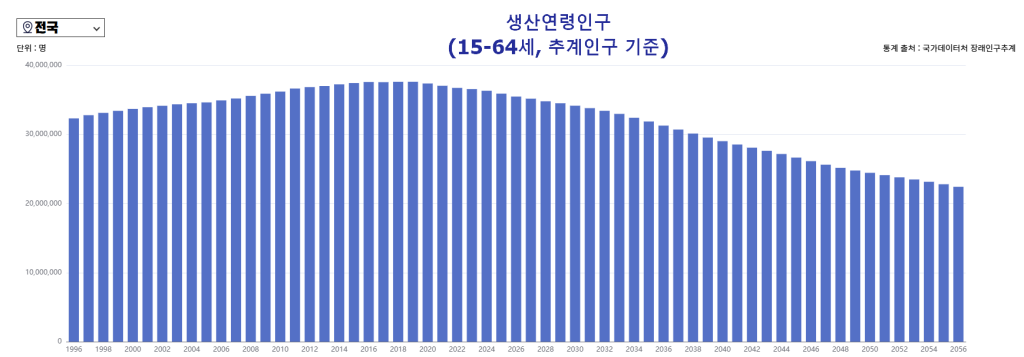

Decline in Working-Age Population: Projections for the working-age population (15-64 years old) show a continuous decline after peaking in the 2020s.

https ://kosis.kr/visual/populationKorea/PopulationDashBoardMain.do

2. 1st Floor (Semi-Basement) National Pension: Realistic Perception of National Pension and the Need for Retirement Supplements

The National Pension should be perceived not as a perfect bulwark for retirement, but rather as a basic financial system with characteristics of compulsory savings and taxation.

As of May 2026, adjustments to the National Pension’s income replacement rate and increases in premium rates are in an unavoidable discussion process. The moment one expects this to be the entirety of their retirement assets, the initiative in financial planning becomes subservient to national policy.

Only when one adopts a ‘semi-basement’ perspective of recovering a portion of the principal paid in, does the motivation to focus on the next layers—retirement pensions and personal pensions—form. While checking one’s basic financial health through the National Pension Service‘s estimated benefit inquiry, it is essential to make conservative estimates within the overall portfolio allocation.

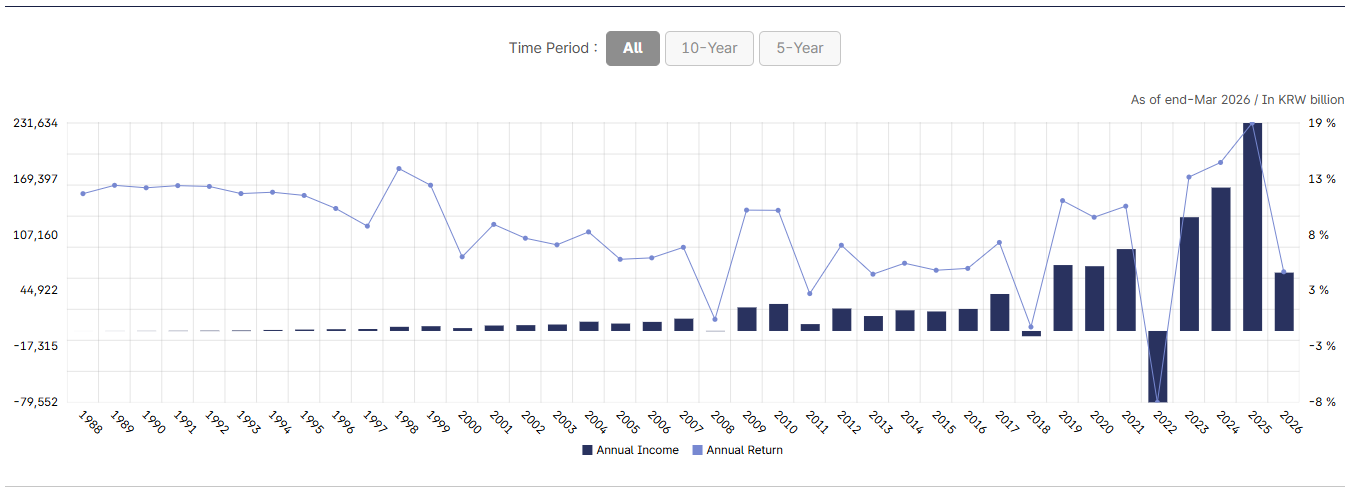

According to official data from the National Pension Service Fund Management Headquarters, the National Pension’s returns fluctuate with changes in the macroeconomic environment. Recent fund management performance shows a negative return in 2022 due to a synchronized decline in global financial markets, but significant achievements were made in 2023 and 2024, driven by market recovery.

Data Source: May 2026 National Pension Service Fund Management Headquarters

Strategic Response Beyond Wishful Thinking

It is true that the additional profit size of the National Pension is numerically increasing. However, one must confront the macroscopic structure of population decline and policy uncertainties hidden behind this numerical growth. In a situation where the demographic structure has collapsed, relying on ‘wishful thinking’ that one will fully receive the same level of benefits enjoyed by previous generations is a very dangerous financial gamble.

Position the National Pension as a minimum defense line, akin to a ‘semi-basement,’ rather than the entirety of your retirement. Then, independently design a robust framework and engine—retirement pensions, personal pensions, and individual stock investments—to implement a proactive asset management strategy that defends your retirement from the volatility of the state system.

Investment Point: The National Pension should be fixed as a retirement defense line with minimized expectations, and the proportion of active investments should be increased.

3. Forming the Framework for Stable Compounding Returns Through 2nd Floor Retirement Pensions and 3rd Floor Personal Pensions

If the National Pension is the foundational base for retirement, then retirement pensions (DC type, IRP) and personal pensions (pension savings funds) are the core rebar that builds the framework of the retirement asset structure. Beyond merely saving cash, one must operate a ‘tax-deferred, stable asset growth system’ that combines tax benefits with compounding returns.

| Account Type | Managing Entity | Key Advantage | Recommended Operating Strategy |

|---|---|---|---|

| Defined Benefit Retirement Pension (DB) | Employer (Company) | Fixed Benefit Level | Stable Asset Management |

| Defined Contribution Retirement Pension (DC) | Individual (Employee) | Employee Manages Employer Contributions | Accumulation mainly via Index-Tracking ETFs |

| Individual Retirement Pension (IRP) | Individual | Tax Credit + Tax Deferral | Mix of Low-Cost Index ETFs |

| Pension Savings Fund | Individual | Tax Deferral + Withdrawal Flexibility | Global Index Asset Allocation |

1) Retirement Pensions and Personal Pensions: Forming the Framework for Compounding Returns

If the National Pension is the foundational base for retirement, then retirement pensions (DB, DC, IRP) and personal pensions (pension savings funds) are the core rebar that builds the framework of the retirement asset structure. Beyond merely saving cash, one must operate a ‘tax-deferred asset growth system’ that combines tax benefits with compounding returns.

2) Retirement Benefit System: The Start of Secure Accumulation

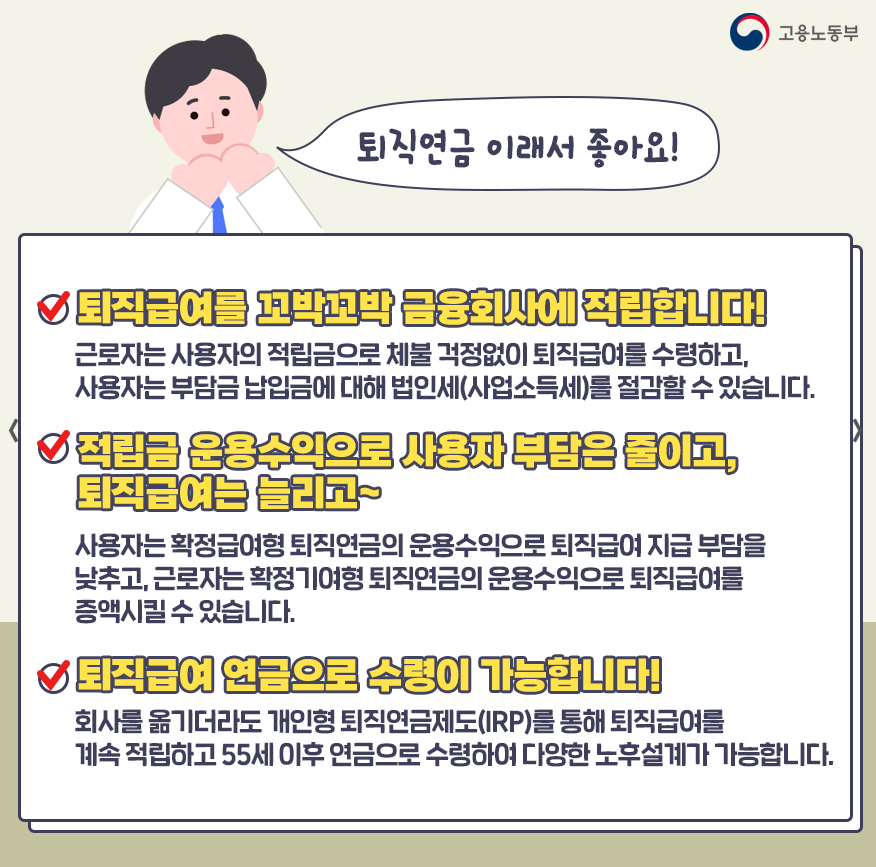

The retirement pension system is a method where employers accumulate and manage retirement benefit funds with external financial institutions, making it much safer and more systematic than a severance pay system managed internally by the company. This ensures employees receive retirement benefits without fear of non-payment, and provides employers with the tangible benefit of corporate tax (business income tax) savings.

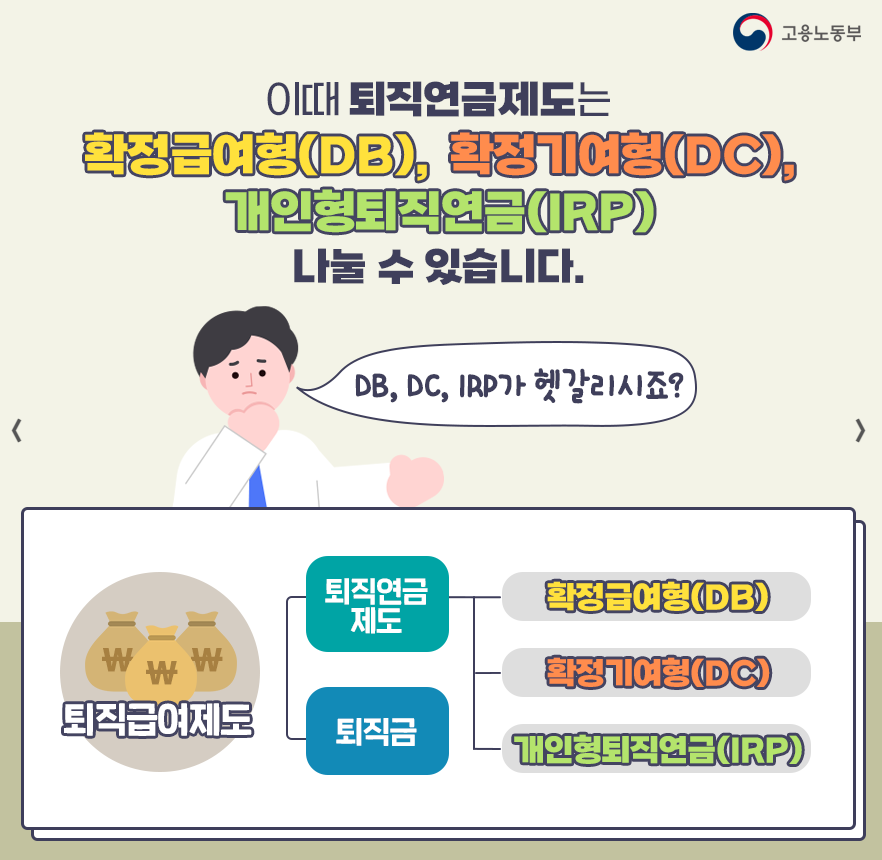

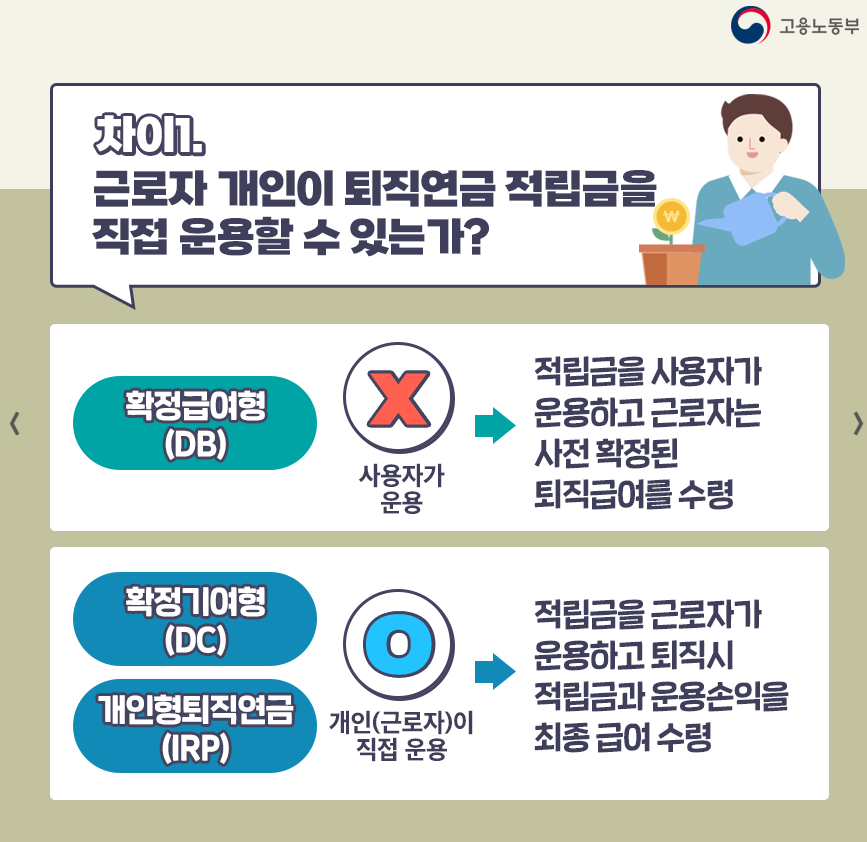

3) Types of Retirement Pensions and Key Differences

The retirement pension system is broadly divided into three types based on its operating method:

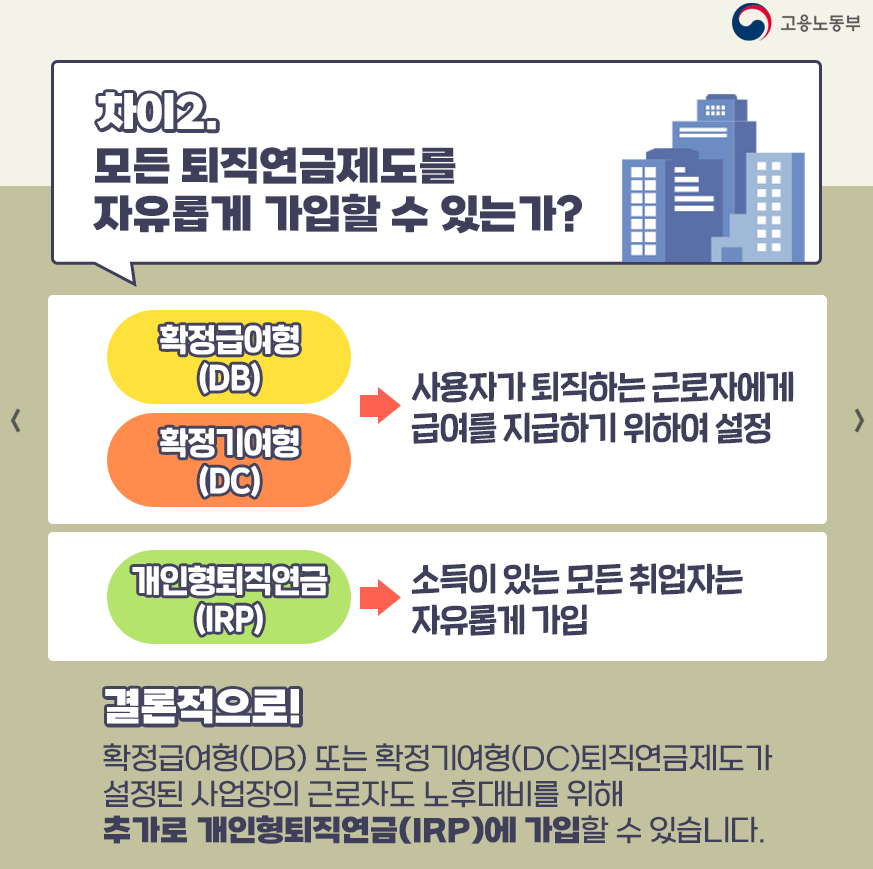

Defined Benefit (DB): The employer manages the accumulated funds, and employees receive a pre-determined retirement benefit upon retirement.

Defined Contribution (DC): Employees directly manage the accumulated funds, and upon retirement, receive the total of the accumulated funds and investment gains/losses as their final benefit.

Individual Retirement Pension (IRP): All employed individuals with income can freely subscribe, and even if they change companies, they can continue to accumulate retirement benefits and receive them as a pension after age 55.

4) Why Pension Accounts? (Tax Benefits and Compounding Effect)

Pension accounts maximize the efficiency of long-term investments through tax credits and tax deferral.

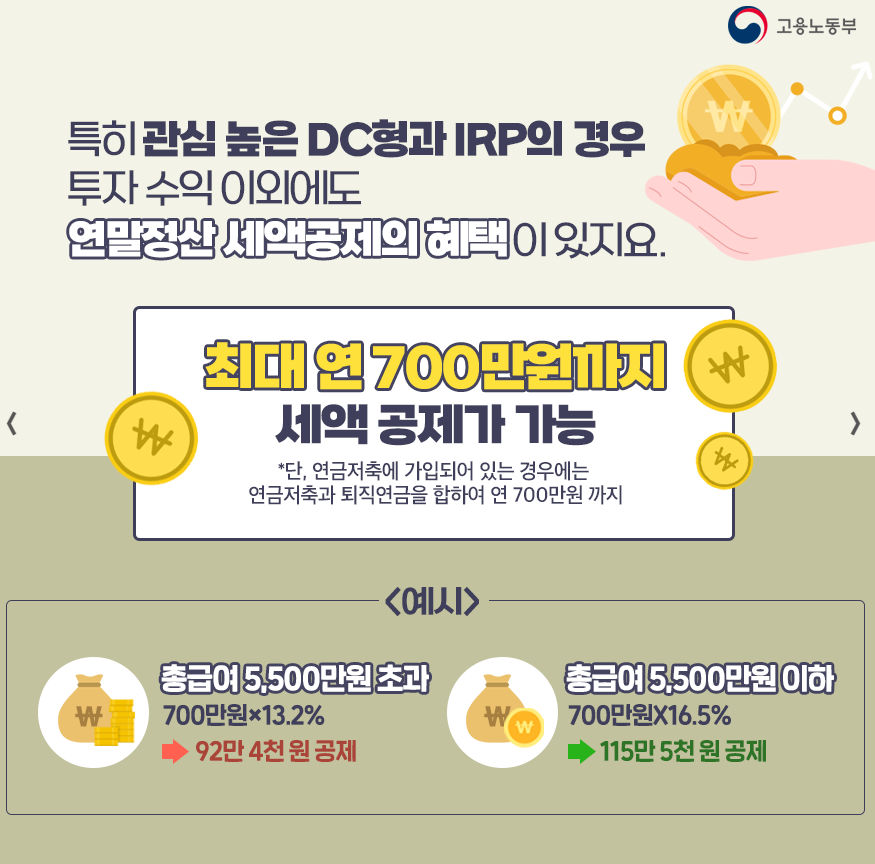

Tax Credit: DC-type retirement pensions and IRPs are eligible for a tax credit of up to 7 million KRW annually during year-end tax adjustments.

For total annual income exceeding 55 million KRW: 7 million KRW × 13.2% = 924,000 KRW credit

For total annual income of 55 million KRW or less: 7 million KRW × 16.5% = 1,155,000 KRW credit

Compounding Effect: Even when profits occur, dividend income tax is not paid each time; taxation is deferred until retirement, and that tax amount is reinvested, dramatically boosting long-term returns.

4) Core Operating Strategy: Index-Tracking ETFs

As of June 2026, the most efficient strategy is to consistently purchase long-term upward-trending global index-tracking ETFs (S&P 500, Nasdaq 100, Dividend, etc.) within pension accounts. Rather than being swayed by the volatility of individual stocks, absorbing the overall market growth rate into your retirement assets through compounding yields the most powerful results in the long run.

| Account Type | Managing Entity | Key Advantage | Recommended Operating Strategy |

|---|---|---|---|

| Defined Benefit (DB) | Employer (Company) | Fixed Benefit Level | Stable Asset Management |

| Defined Contribution (DC) | Individual (Employee) | Investment Gains Attributed to Employee | Accumulation mainly via Index-Tracking ETFs |

| Individual IRP | Individual | Tax Credit + Pension Withdrawal | Mix of Low-Cost Index ETFs |

5) Investment Points

Control over Management: DC-type and IRP accounts allow individuals to directly manage their accumulated funds, thereby increasing retirement benefits through investment gains.

Leverage of Time: Focus on dollar-cost averaging into the market’s upward trend during the remaining period until retirement, lowering the average cost and securing more units.

Robust Framework: For this layer, ‘mechanical and continuous investment’ through automatic purchase settings, rather than emotional investing, is the key to success.

4. Individual Stock Investment: The 4th Floor Engine for Accelerated Growth

If the National Pension (1st floor or semi-basement) establishes a minimum defense line, and retirement pensions and personal pensions (2nd-3rd floors) build the framework for stable compounding growth, then a ‘growth engine’ is now needed to dramatically boost the overall portfolio’s returns. Individual stock investment, the 4th floor, is an aggressive strategy to accelerate the quantitative growth of total assets.

1) Why the 4th Floor Engine?

If index investing within pension accounts is a safe voyage following ‘market averages,’ then 4th-floor individual stock investing is a process of pursuing ‘excess returns (Alpha)’ by selecting companies that lead technological dominance and industrial change. This engine functions properly only when a stable underlying structure is secured, expanding asset size based on the capacity to withstand volatility.

2) 2026 Strategy: Focus on Technological Dominance and Value Chains

As of June 2026, AI infrastructure and energy dominance, which are fundamentally changing the industrial landscape, are the areas that demand the most attention.

AI Infrastructure: Semiconductor design and manufacturing companies that provide the essential computing power for the proliferation of generative AI offer powerful momentum to the portfolio.

Power Infrastructure: Power equipment and energy solution companies that will address the explosively increasing electricity demand for AI data center operations are key value chains for technological dominance.

3) Operating Principles: Strategic Discipline and Risk Management

4th-floor investment is an engine that accelerates asset growth, but it comes with excessive volatility. Therefore, the following strict principles must be presupposed:

Weight Limit: Strictly control the proportion of individual stocks within the overall retirement asset portfolio to prevent a market crash from leading to the collapse of the entire retirement fund.

Value-Oriented Selection: Focus on market-dominant companies that possess an industry moat and overwhelming technological superiority, rather than speculative investments chasing trends.

Observation of Market Changes: The 4th floor is an area that requires regular rebalancing. Continuous analysis of changes in the industry’s value chain is necessary to maintain the engine’s performance.

4) Investment Points

Accelerated Growth: If the 1st-3rd floors are defensive assets, the 4th floor clearly functions as an aggressive asset that expands the size of the asset pie.

Securing Technological Dominance: Investing in leading companies in industries poised for growth for the next 10+ years, such as AI and energy, is a strategy to preemptively capture future value in the present.

Psychological Buffer: The more robust the underlying structure (pension accounts), the less one is swayed by the fluctuations of individual stock investments, allowing for a longer-term perspective to await corporate growth.

[Summary] 4-Stage Roadmap for Retirement Assets

1st Floor or Semi-Basement (National Pension): Acknowledging the demographic crisis and managing conservatively as a minimum defense line

2nd-3rd Floors (Retirement/Personal Pensions): Building a framework for compounding returns by combining tax benefits and index ETFs

4th Floor (Individual Stocks): An engine to accelerate asset growth through technology-dominant investments

Through this multi-layered structure, readers can transcend the uncertainties of national policy and embark on a proactive asset management path to defend and enrich their own retirement. This systematic design today will be the most powerful weapon in determining your financial freedom 20 or 30 years from now.